Let’s Disrupt Wealth Inequality—Starting Right Now In Your Community

A doable strategy for every city and town in America

What to Expect

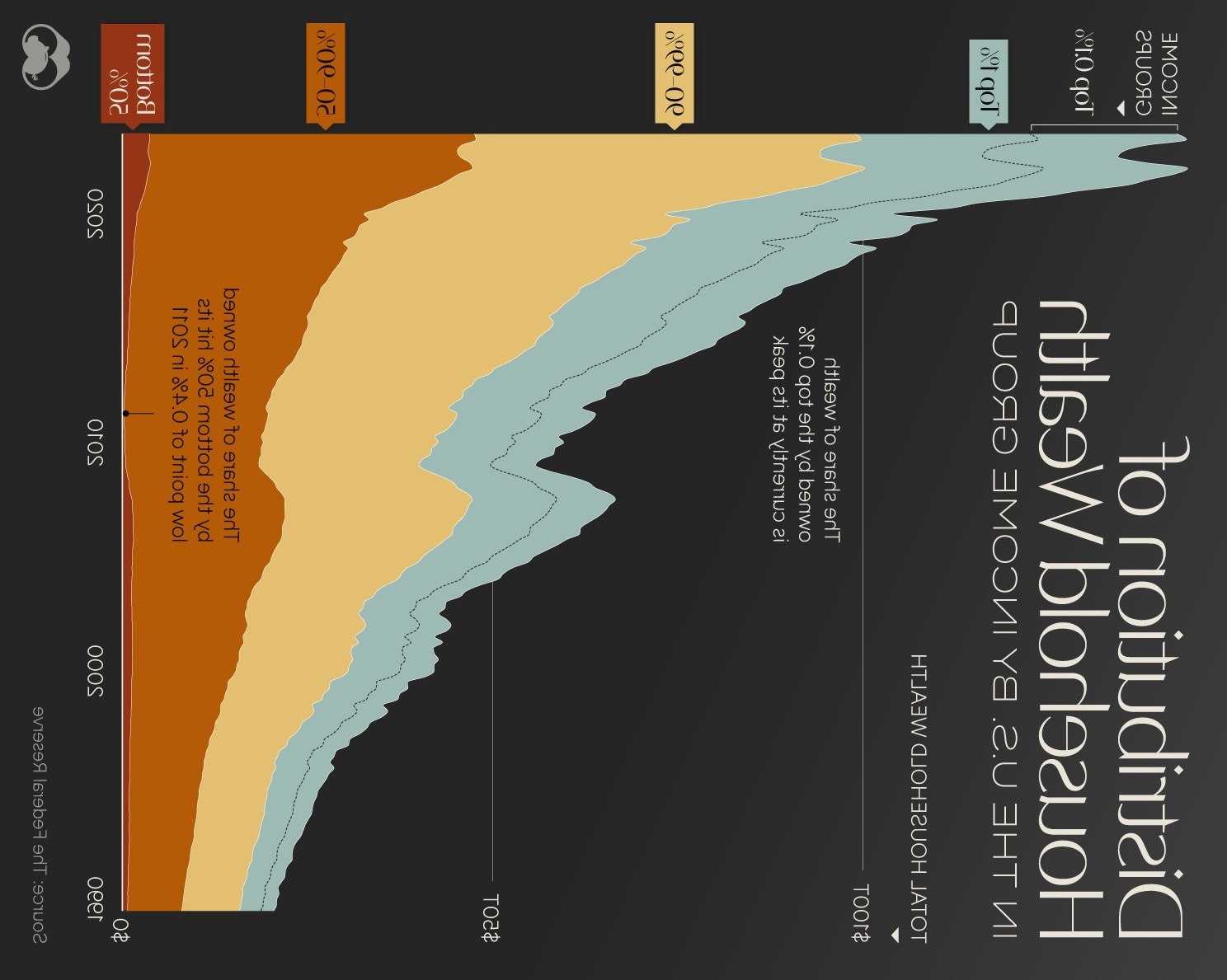

Multigenerational poverty and wealth inequality is and has been causing massive amounts of harm to American families and children for generations, with adverse ripple effects throughout the economy that are only accelerating and worsening with each passing year.

Many of us feel powerless to do anything about it. But together, we can have a life-changing impact on people in our community, especially children and young people—but the strategies need to be feasible and effective.

Below I propose a practical strategy that nearly every community in America can implement—right now—to begin disrupting wealth inequality.

I also describe how the strategy works and provide a customizable program outline to help communities get started.

The Observable, Demonstrable, Known Thing

I’m not going to belabor this point with an extended list of linked references, statistics, and research—just google some things because the evidence is abundant and observable everywhere you look:

Economic inequality is bad.

Now moving on…

Change What You Can

You don’t have to be an economist to take economic action to counteract inequality.

Most of us believe we cannot do much of anything to solve our massive macroeconomic problems, such as unstoppable national indebtedness, rampaging capitalist pillaging, absurdly ballooning healthcare costs, mountainous piles student-loan debt, swirling storms of unaffordability spiraling in fractals all around.

Consequently many of us feel helpless, often most of the time, particularly lately.

But we can have a microeconomic impact, particularly on individuals, and especially on children and young people, people who then become the adult contributors to our economy.

And if enough children and young people are positively impacted, starting as early prekindergarten, positive macroeconomic impacts will follow, even if they take years or decades to manifest.

And when solutions take years or decades to manifest, the best approach is to get started immediately.

One of my operative principles:

If you can’t change something, change something you can.

A Community-Based Disruption Strategy

In these times of overwhelm and learned helplessness, we need practical, feasible strategies that a few dozen, a few hundred, or a few thousand people can enact in their sphere of influence with the knowledge, skills, resources, and money they have.

This community-based strategy will never solve everything, and it won’t have an immediate impact on large-scale problems, but it can be an invaluable contribution to the solution, a contribution that millions of people could make right now, and it will have a direct, lasting, and possibly even life-altering impact on some proportion of the young people and families involved.

Here’s the strategy that nearly every community in America can implement—starting right now—to begin disrupting wealth inequality:

Step 1. Start with these three facts: Nearly half of households in America have no retirement savings, more than 30% have less than $25,000 saved, and more than 20% have zero savings. Specific data sources and statistics vary a bit, but who cares? The situation is demonstrably very not good at all, and the fallout is observably obvious everywhere.

Step 2: Identify the mechanisms of change. Disrupting multigenerational poverty and wealth inequality begins with (a) some financial knowledge, (b) some amount of financial guidance and mentoring, and (c) some money. And the earlier this support is provided in someone’s life, the greater the potential impact will be over the course of their lives.

Step 3. Establish a clear, feasible, unambiguous objective. In this case: If we give as many 18-year-olds as we can (a) some financial knowledge, (b) some amount of financial guidance and mentoring, and (c) some money to invest in a retirement account, particularly young people in our poorest households, it will increase rates of retirement investment by more young adults in our country, by some amount, in direct proportion to the number of young adults who receive the support, dramatically increasing their net worth and retirement security over time. My recommendation is to provide a+b+c in the community where they live, while they are still a captive, reachable, co-located audience—i.e., when they’re in high school.

Step 4. Design the program. You don’t need to start from scratch! I’ve provided a customizable program outline below to help communities get started.

Step 5. Recruit a team of coordinators, fundraisers, funders, educators, and volunteers. The amount of funding required to operate the program will be proportional to the number of young people supported, but the program can be implemented with a relatively small team of people and a relatively small amount of locally raised funding. Ideally, the program will be managed by at least one person who is being paid for their time—it could be a teacher, a nonprofit or municipal employee, or a loaned employee from a bank or other local business. It could also be coordinated by an education foundation or PTO volunteer, or a retired person with relevant skills. Other volunteers will be needed, but their overall time investment will likely be relatively minimal, manageable, and short-term.

Step 5. Secure donations to fund starter Roth IRA accounts. This step is vital. In fact, it’s essential to the strategy’s success: Give young people money to invest in an individual Roth IRA retirement account. The strategy encompasses three primary tactics: (1) provide retirement education, (2) open retirement accounts, and (3) fund retirement accounts with seed money. This is the linchpin of the strategy, and what sets this strategy apart from other strategies. Helping young people open a retirement account (not just telling them to do it) and giving them some money to invest (not just telling them to invest on their own) will dramatically increase both participation rates and long-term impact. Relative to the number of students involved, the seed money required to open and fund an individual Roth IRA will, of course, increase proportionally. Some major brokerage firms allow investors to open an online retirement account in minutes with $0—i.e., a lack of money is not a barrier to opening an account, and some firms allow investors to start with as little as $1. While it would be amazing if a community could give every high school graduate $500 or $1,000 to invest, any amount of funding will be better than nothing. If the graduating high school class is 350 students, it will require $35,000 to deposit $100 in each account, $17,500 to deposit $50, and $3,500 to deposit $10. One donor, philanthropy, local education foundation, or modest fundraising campaign could raise $35,000 in most communities that produce 350 high school graduates each year. A few banks could easily contribute this amount, many of them already have philanthropic community programs, and this strategy dovetails with their business model, their employees’ skill sets, and their charitable missions. Many communities give out tens or even hundreds of thousands of dollars in scholarships each year to a small number of graduates (who often need the money the least), and one mid-sized philanthropic foundation could give $50,000 or $100,000 to the program. Giving every graduate a “Roth IRA scholarship” might not help them pay for college, but it will capitalize a retirement account that could be worth hundreds of thousands decades from now. Raise as much money as you can, divide it up equally, and dump it in there.

Step 5. Encourage young people and their families to match the investment. Some families have more than they need, and some don’t have enough. All participating young people should be offered the same amount of seed funding, regardless of household wealth or income, but families with greater financial means can be given the option to donate extra money to the cause and/or redistribute their child’s portion to other young people who need it more—and their children can still benefit from other elements of the program (financial education, assistance opening an account). Some young people might have money to contribute from a part-time job, and they should be encouraged to contribute something, even if it’s only a small amount. Their parents can also make a matching contribution at whatever level they are able. Parents in the community will also know many of the young people who will benefit, and parents of means who donate to the program will be giving money to kids they know. People are more inclined to give money to individuals, especially people they know, particularly when those people will directly benefit, in visible ways, from their financial support. Local news coverage, an article in the schools newsletter, or a celebratory public event at the conclusion of the program will elevate visibility and awareness, and contribute to the long-term sustainability of the program in subsequent years by attracting more attention, volunteers, and donations.

Step 6. Invite and involve parents. Multigenerational poverty and inequality is multigenerational—the adverse effects get passed on from one generation to the next. In many cases, the families of participating young people will have received no financial education, mentoring, or support at any point in their lives. If the program is already going to be educating their children, why not invite them along for the ride? Communities could also run an adult program in tandem with the youth program, and even hold it in the same location at the same time. The parents can attend the educational experiences alongside their children, and they can be there when a volunteer helps their child open their Roth IRA account. If the child is under the age of 18, parents or guardians should be there anyway. If some proportion of participating parents also decide to open retirement accounts, you’re slathering gravy on top. The positive effect will be doubled without requiring twice the investment.

Step 7. Explore options for cross-program integration. In many communities, programs may already exist that dovetail with the strategy. Operationally, the program could be integrated with another program to streamline coordination, leverage existing volunteers, and increase fundraising and impact. For example, the AARP and United Way offer free community-based programs that help people file their taxes. Taxes are filed in the spring, and the program can be implemented in the spring semester of senior year. The people volunteering their time to a tax-preparation program have financial expertise, and they have already demonstrated their desire to volunteer their time to help people out financially in their community. If a community-based, tax-preparation program already exists, the existing programmatic infrastructure—compensated coordinators, organized volunteers, suitable locations—could be leveraged to reduce the overall investment required to design and run the program.

Step 8. Build out and refine the program over time. Once the program model has been built and implemented once, operating the program in each subsequent year will require less investment than it did the previous year, particularly if the model worked well and adult volunteers keep returning year after year. If a virtuous cycle takes hold, the result will be more volunteers, more support and mentoring for young people, and more money year over year, and it will take less time and energy to manage the program.

A Starter Program Design

Objective

Provide all high school seniors with a financial education and mentoring experience, help them open a retirement account, and give them a modest monetary gift to fund their new account.

Programmatic Components

Provide an accessible educational experience. The learning experience could take place during school, after school, or on a weekend. It could be offered as an extension of an existing high school course or community program, or it could be offered as a standalone program. It could be one session or multiple sessions, but it doesn’t need to be an intensive weeklong course. For example, participating young people could receive 3-4 hours of group instruction, and 1-2 hours of support to open their account at a different time by a team of volunteers. People are busy and distracted, so shrink it down to the most important essentials to make it more feasible, increase participation, and get it done.

Keep it simple and executable. Focus the experience on the highest-priority basic financial knowledge. Don’t overbuild the curriculum or overthink the process. Don’t make the planning, organization, and coordination needlessly complex and cumbersome. Don’t give young people or volunteers reasons to not show up and participate. Getting people there and getting it done matters far more than getting it perfect.

Find at least one program coordinator. The program can be coordinated by the school, a nonprofit, an education foundation, a PTO, or a for-profit partner. If you keep it simple, one person working on the program for 10–15 hours a week over a month or two could organize the entire soup to nuts. Pick an organization that’s mission-aligned and already knows how to manage community-based programs.

Develop a simple, easy-to-execute curriculum. For the curriculum, I recommend something like this:

Give each young person a copy of I Will Teach You to Be Rich by Ramit Sethi (usually purchasable for around $10–$15). Don’t buy copies from Amazon—work with a local bookstore to bulk-order copies at a significant discount. The book is breezy and easy to read, it provides a step-by-step program, it’s written for young people, and it’s formatted to be more approachable for those who are less inclined to read long-form books. It also conveys the practical, foundational financial information everyone should know—not blizzards of unimportant technical minutia.

Use the book to structure the curriculum and learning experience. Here’s a PDF of the table of contents and first chapter. Pick the most important lessons from each chapter, boil it down into a mini-course and presentation, and walk students through the lessons using engaging visuals and concrete, real-world examples. Give a stipend to a few teachers who know what they’re doing to design the curriculum and instructional strategy, and teach the mini-course.

Consider holding learning sessions in a central community space, particularly if some students have negative associations with the high school. Pick a nice and inviting location, such as somewhere that’s light-filled and beautiful. Host it at a bank, college, corporate headquarters, or other professional setting that brings young people into a space they would not get to experience otherwise. Communicate: You deserve good things, you belong here, you could work here one day, you have options and the personal agency to change the course of your life.

Keep the learning experience short, interesting, and fun. Don’t drone on. Be energetic and funny. Keep it zippy and light, but also convey the enormous importance of making sound money decisions, and how unsound financial decisions can adversely impact their lives in profound ways. Keep it real—no economic abstractions or financial jargon. Connect the lessons to their interests, their aspirations, and their actual lives. Have the adults in the room share their personal experiences with money, particularly the mistakes they made, and why and how they changed course. Bring in a charismatic speaker who will resonate with them, such as an alum who became a noteworthy person or someone like them who built some wealth from nothing. Share specific examples of non-rich people making good decisions that put them on the path to wealth-building.

Above all, educate them about compound interest. Show them the numbers—i.e., the wealth they could end up with in 40 years if they follow a few simple rules, invest X annually, and keep contributing as much as they can every month, even if some months it’s only $10 because that’s all they can manage that month.

Enlist relevant parties. Teachers know how to teach. Nonprofits and philanthropies know how to run programs. Accountants and bankers know about money and how to open online accounts. Retired people who worked in the finance sector may be sitting around on their large nest eggs looking for something to do.

Help the students open a Roth IRA account. Don’t just tell them how to do it—show them how to do it by doing it with them. Sit down next to them, open the browser, walk them through the process, transfer the money in, and then hand them a lollipop before they walk out the door. Volunteers can help the young people set up the account, then hand off the process to someone who will transfer in the seed money.

Find banks to work with. I suspect the most efficient way to manage the money is to put all the donations into a bank account (or multiple accounts if multiple banks are involved). From that account, individual contributions can be transferred out. If bank employees manage the transfer, the bank can oversee the process to ensure that mistakes are not made. This part of the process will require some troubleshooting, conditions will vary from community to community, and legal issues might be involved (e.g., if the young person is a minor), so figure out what works.

Fund the accounts with seed money. I do not recommend handing young people or families a check and letting them take it from there. If this is the only way to get it done, move forward, see what happens, and try something else the following year if it doesn’t work. With that said, I strongly recommend transferring funds directly into the retirement accounts because young people are still young, and for some the temptation will be irresistible to spend that money on something other than the abstract prospect of a larger amount of money decades in the future (particularly for those young people who are not accustomed to having money to spend). One option might work like this: The young person is given a check on the condition that it is invested in a retirement account, a local bank works with them to open a savings account (if they don’t already have one), and the money is transferred from that account into the retirement account and invested a fund at the time it’s opened. Make sure the money is actually invested, not just sitting there uninvested in a brokerage account—this is another reason why someone should help the young people involved open and fund the account.

Only invest in low-cost index funds—no exception. Avoid all high-fee funds and invest donated funds exclusively in diversified, low-cost, passively managed index funds that hold thousands of diversified U.S. stocks across all sectors and market capitalizations, such as a total stock market fund. I specifically recommend Vanguard’s target date funds. Target date index funds are “set-it-and-forget-it” retirement investment vehicles that automatically adjust their “asset allocation”—as investors approach a specific retirement year, the portfolio gradually shifts from a higher percentage of high-growth stocks (more risky, higher potential returns) to a higher percentage of conservative bonds (less risky, lower return). Vanguard’s fees are extremely low, the target-date portfolio is self-managing (no stock-market knowledge required), and the funds perform as well as or far better than the best investment vehicles out there. It’s a simple one-decision, one-vendor strategy, and if participating young people did nothing else over the course of their adult life but invest consistently in a Vanguard target date fund, they would likely be sitting pretty at retirement (barring a global financial crash, of course).

Beware of financial advisors. Many financial advisors are not legitimate advisors—they are salespeople selling the financial products they are paid to sell. And the “products” they sell are often high-priced funds that perform horribly compared to low-cost, broad-market index funds. A huge proportion of financial advising activity in the United States is a scam—so do not let scammers scam young people in your community, period. It would be unethical and irresponsible to expose young people and families to self-dealing financial advisors with ulterior motives. The business model is predicated on bringing in new clients who don’t realize (1) they can do it themselves for free and get better results; (2) the management fees charged by the advisor or brokerage firm are exorbitant; (3) even small annual fees, negatively compounded over 40 years, could potentially drain off hundreds of thousands from a retirement account; and/or (4) the financial products they sell nearly always underform the diversified, low-cost index funds that track the market. Even financial advisors who are “fiduciaries” will sell garbage and hand out bad, self-serving advice without disclosing conflicts of interest. I have friends and family who have personally experienced the consequences of unethical financial advising, with devastating financial consequences). If some financial advisors want to volunteer, that’s great—but do not let them sell anything to anyone involved. No exceptions. Do not ask them to recommend investment vehicles; do not involve them in the coordination if they are unable to abide by the rules. If they attempt to sell themselves or their products to anyone involved, at any time, ask them to leave immediately and don’t welcome them back.

Spread the word and help out other communities. If you come up with tactics that work—how to recruit young people and their families, how to manage elements of the program, how to design an effective learning experience—share your model with other communities and help them get their own program off the ground. Present the program at professional conferences and offer webinars. Schools are often risk-adverse, and for good reason—whenever they make a mistake, even a small one, they get hammered by everyone. This is why many districts and schools often wait until other districts and schools in other communities do something that works.

Consult a lawyer. To make sure the programmatic details are legal, and particularly as they relate to legal minors, consult a lawyer. You may want to require parents or guardians to be present during the account set-up process. I don’t know if there are any potential legal concerns entailed in anything I’ve described above, so ask a local law firm to review the program (ideally pro bono).

Don’t let a small amount of risk torpedo a life-changing opportunity for young people. Accept that every new venture entails some amount of risk. If money is involved and adults are helping young people set up investment accounts, parents will want to know that the people involved can be trusted. That’s why I recommended working with trusted institutions like banks, and operating the program in partnership with a high school or credible, well-known local nonprofit.

I’m hoping to get one of these projects off the ground as I write these words. If you want some help, or if you are a foundation interested in funding the work in your community or region, send me an email.

~SEA

Last revised 2.17.26